Mistake #4: Indiscriminate Cost-Cutting Programs

- Dr. Marvilano

- Sep 1, 2018

- 7 min read

This blog post is part of the Seven Fatal Mistakes of Cost-Cutting series. Don't have time to read it now? Download the PDF here.

The Problem: Indiscriminate Cost-Cutting Programs

Cost-cutting programs are often viewed as a necessary step to improve financial performance and increase profitability. However, when cost-cutting measures are implemented without a balanced approach, it can lead to disastrous consequences for the company. Some companies fall into the trap of cutting too much, failing to differentiate between good costs and bad costs. In this section, we will explore the problem of cost-cutting programs that go too far, hampering the company's ability to compete, grow, and run its operations efficiently.

Failure to Differentiate Good Costs and Bad Costs

One of the major pitfalls of excessive cost-cutting is the failure to differentiate between good costs and bad costs. Good costs are investments that contribute to the long-term growth and competitiveness of the company. These expenses may include research and development, employee training and development, marketing, and technology upgrades. Cutting these good costs can hinder the company's ability to innovate, maintain a competitive edge, and adapt to changing market demands.

Hampering Business Competitiveness

Excessive cost-cutting, especially when it involves slashing investments in critical areas, can hamper the company's ability to remain competitive in the market. For instance, reducing marketing expenses might lead to decreased brand visibility and customer engagement, causing a decline in market share and revenue. Similarly, underinvesting in research and development can leave the company ill-equipped to develop new products or improve existing ones, allowing competitors to gain an advantage.

Impeding Growth Opportunities

Cutting too much can also impede the company's growth opportunities. Expansion into new markets, launching new products, or making strategic acquisitions may require upfront investments that could be viewed as "costs" in the short term. However, failing to make these necessary investments may hinder the company's ability to capture new opportunities and expand its market presence.

Undermining Operational Efficiency

While cost-cutting aims to improve efficiency, excessive measures can have the opposite effect. For instance, reducing staff to save costs might lead to increased workload and decreased employee morale, resulting in decreased productivity and operational inefficiencies. Cutting back on necessary maintenance or infrastructure upgrades can also lead to increased downtime and operational disruptions.

Sacrificing Customer Experience

Excessive cost-cutting can also have a detrimental impact on the customer experience. For example, reducing customer service resources might result in longer wait times and less personalized support, leading to dissatisfied customers and potentially lost business. Sacrificing the quality of customer experience can harm the company's reputation and erode customer loyalty.

Impact on Employee Morale and Retention

Cost-cutting programs that go too far can significantly impact employee morale and retention. Layoffs and wage freezes may create an atmosphere of fear and uncertainty among the workforce, leading to reduced engagement and increased turnover. Losing valuable talent can have a negative effect on the company's ability to innovate and execute its business strategies effectively.

Neglecting Long-Term Viability

Excessive cost-cutting often focuses on short-term financial gains while neglecting the company's long-term viability. Investments in employee training, process improvement, and infrastructure upgrades may be seen as costs in the short term but can lead to significant returns in terms of efficiency, productivity, and overall performance in the long run. Failing to make these necessary investments can hinder the company's ability to remain competitive and sustainable over time.

Missed Opportunities for Profitable Growth

Ultimately, cutting too much can lead to missed opportunities for profitable growth. By overly prioritizing cost reduction, companies may overlook strategic investments and partnerships that could have yielded substantial returns. As competitors seize these opportunities, the company's growth potential may be compromised.

The Root Cause: Failure to Differentiate Good Costs from Bad Costs

While cost-cutting is essential for financial efficiency, the failure to differentiate between good costs and bad costs can lead to the pitfalls of excessive cost-cutting. Companies must discern which costs are necessary to run operations efficiently, maintain competitiveness, and drive growth, and which costs are merely wasteful spending. The inability to make this crucial distinction can expose executives to the risk of destroying the company with an overly aggressive cost-cutting program. In this section, we will explore the root causes of this problem and the challenges it poses to effective cost management.

Lack of Cost Visibility and Transparency

A fundamental cause of the problem lies in the lack of cost visibility and transparency within the organization. Without a clear understanding of how costs are allocated and how they contribute to various aspects of the business, executives may struggle to differentiate between essential and non-essential expenses. Insufficient data and information can lead to uninformed decisions, potentially resulting in the cutting of necessary costs or the retention of wasteful spending.

Short-Term Financial Pressures

Short-term financial pressures and the need to meet immediate financial targets can drive companies to pursue aggressive cost-cutting measures without adequate consideration of the long-term consequences. Executives facing external pressures from investors or stakeholders may prioritize short-term savings over investments in strategic areas, risking the company's competitiveness and growth potential in the future.

Inadequate Strategic Planning

A lack of robust strategic planning can also contribute to the failure to differentiate good costs from bad costs. When companies lack a clear and well-defined strategy, it becomes challenging to identify which costs are aligned with strategic objectives and which are not. Without a strategic roadmap, executives may resort to across-the-board cost-cutting, neglecting critical investments needed to support the company's long-term goals.

Misaligned Incentive Structures

In some cases, incentive structures within organizations may inadvertently encourage excessive cost-cutting without considering the impact on long-term viability. Executives or managers may be rewarded based solely on short-term financial gains, leading them to prioritize immediate cost reductions without evaluating the potential consequences for the company's overall performance.

Overly Simplistic Approaches to Cost-Cutting

Companies that adopt overly simplistic approaches to cost-cutting, such as across-the-board percentage reductions or arbitrary cost targets, risk cutting both good and bad costs indiscriminately. These one-size-fits-all approaches fail to consider the unique cost structures and value drivers of different departments and business units, leading to suboptimal outcomes.

Resistance to Change and Fear of Risk

Fear of risk and resistance to change can deter executives from making the necessary investments in areas that might be perceived as "costs" in the short term but are essential for long-term success. Executives may prioritize maintaining the status quo to avoid disruption, even if it means forgoing investments that could drive growth and competitiveness.

Siloed Decision-Making

Decision-making that is siloed and lacks cross-functional collaboration can also contribute to the failure to differentiate between good and bad costs. When departments or business units make cost-cutting decisions in isolation, they may overlook the broader implications for the organization as a whole. This fragmented approach can lead to suboptimal cost-cutting strategies that do not align with the company's overall goals.

Lack of a Holistic Cost Management Culture

A lack of a holistic cost management culture that emphasizes the importance of cost optimization and aligns it with strategic priorities can exacerbate the problem. When cost management is not integrated into the organizational culture and decision-making processes, it becomes challenging to make informed and balanced cost-cutting decisions.

The Solution: Understanding Strategy and Competitive Advantage

To avoid the pitfalls of excessive cost-cutting and differentiate between good costs and bad costs, companies must focus on understanding their strategy and drivers of competitive advantage. The key to achieving optimum costs lies in making informed decisions that align with long-term goals and support the company's ability to compete and grow. Instead of solely pursuing minimum costs, companies need to adopt a more strategic and holistic approach to cost management. In this section, we will explore the key recommendation of properly understanding strategy and competitive advantage to distinguish between good and bad costs.

Define Clear Strategic Objectives

The foundation of understanding good costs and bad costs lies in defining clear strategic objectives. Companies need to have a well-defined strategic plan that outlines their long-term goals, market positioning, and value proposition. By understanding their direction and the core areas of focus, executives can prioritize investments that contribute to achieving these objectives, while eliminating or optimizing costs that do not align with the strategy.

Identify Core Drivers of Competitive Advantage

To differentiate good costs from bad costs, companies must identify their core drivers of competitive advantage. These are the unique attributes or capabilities that set the company apart from its competitors and contribute significantly to its success. By understanding their competitive advantage, companies can prioritize investments in areas that strengthen these differentiators, while minimizing expenses that do not directly contribute to their market leadership.

Conduct Comprehensive Cost Analysis

Properly understanding costs requires a comprehensive cost analysis. Companies need to go beyond surface-level evaluations and conduct in-depth assessments of their cost structure. This includes identifying direct and indirect costs, fixed and variable costs, as well as understanding the cost drivers within each department or business unit. A granular cost analysis provides insights into cost efficiency and informs decisions about where cost reductions are feasible without compromising strategic priorities.

Implement Activity-Based Costing (ABC)

Activity-Based Costing (ABC) is a valuable tool for understanding the true cost of activities and processes. Instead of relying on traditional cost allocation methods, ABC assigns costs based on the resources consumed by each activity. This approach provides a more accurate picture of the cost of goods and services and helps identify areas where cost optimization is most impactful.

Adopt Zero-Based Budgeting (ZBB)

Zero-Based Budgeting (ZBB) is another valuable approach to ensure that costs are aligned with strategy. By starting each budget cycle from ground zero, ZBB requires justification for every cost item, forcing departments to evaluate the value and impact of each expense. This approach encourages a more thoughtful and strategic budgeting process and reduces the risk of cutting necessary costs.

Foster Cross-Functional Collaboration

Understanding good costs and bad costs requires cross-functional collaboration. Different departments and business units must work together to identify synergies and opportunities for cost optimization. Collaborative efforts facilitate the sharing of insights and perspectives, enabling better-informed decisions about cost allocation and reduction.

Balance Short-Term and Long-Term Considerations

Cost management should strike a balance between short-term and long-term considerations. While cost-cutting may be necessary for immediate financial objectives, it should not compromise the company's ability to invest in strategic initiatives that drive long-term growth. A holistic approach to cost management considers both the immediate needs and the organization's future aspirations.

Continuously Monitor and Adjust

Understanding good costs and bad costs is an ongoing process. Companies should continuously monitor their cost structures, evaluate the impact of cost-cutting measures, and adjust strategies as needed. Regularly reassessing costs in light of changing market conditions and strategic priorities ensures that cost management remains aligned with the company's evolving needs.

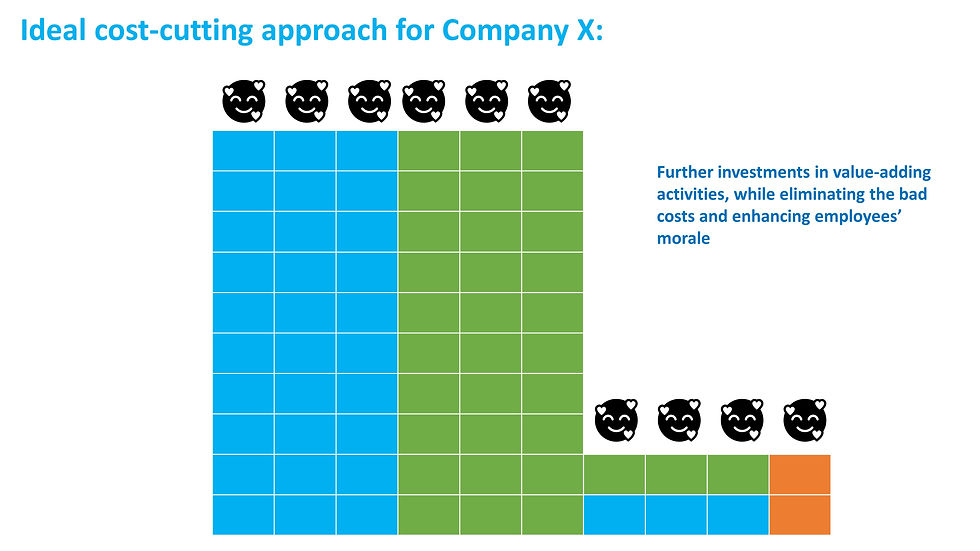

NOTE

Having examined the visuals of misguided cost-cutting decisions, it is essential to understand what the ideal approach should look like. The visual below illustrates the key elements of an effective cost-cutting strategy:

Comments